European cashback cards are noisy because the headline rate is rarely the real rate. A 3% or 5% card can hide a token requirement, a subscription, a reward cap, or an FX charge that matters more than the banner number. The clean version of this question is simple: if you want everyday card spend to become BTC, which European card gives you the least operational drag?

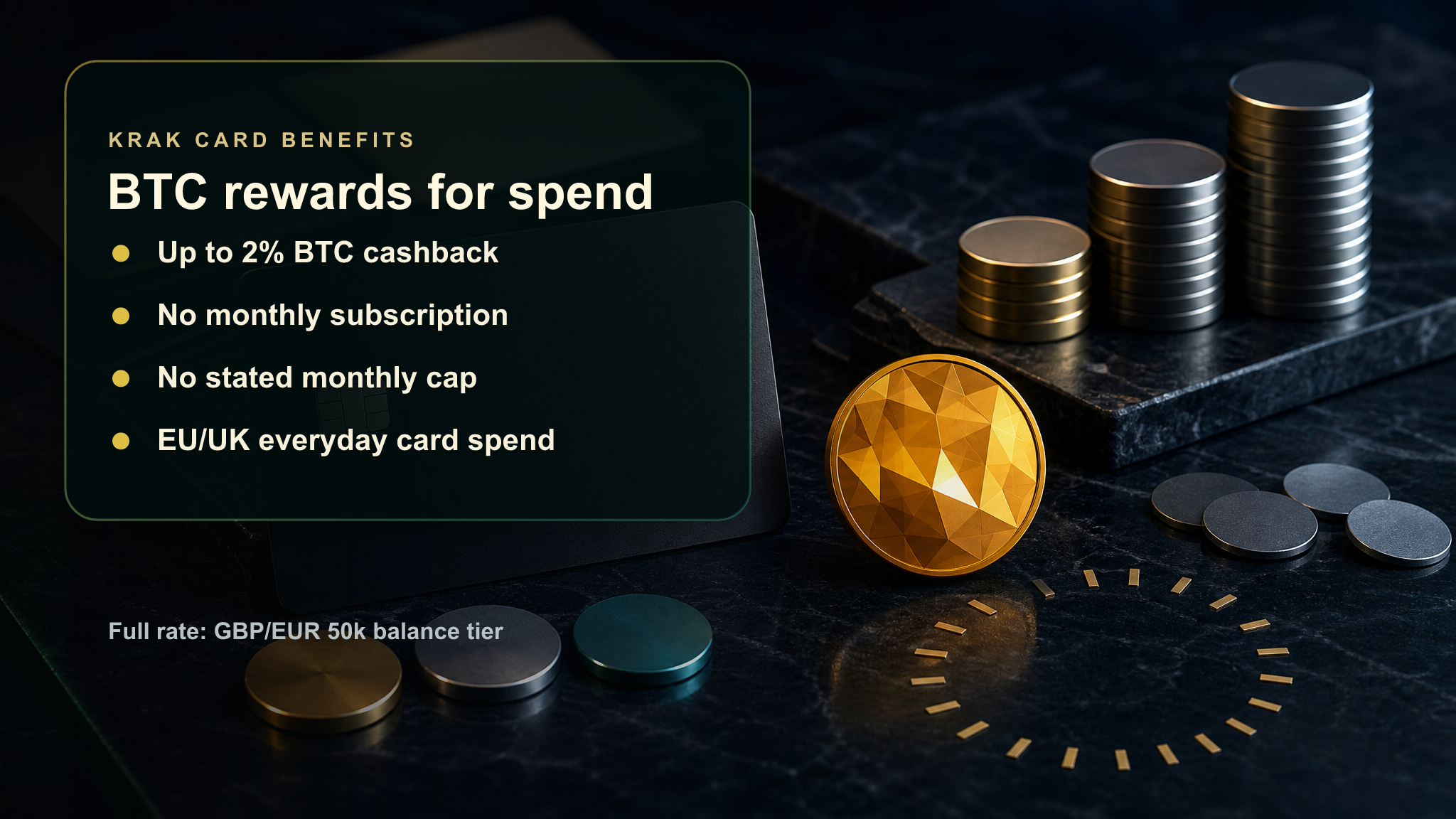

For that specific use case, Krak is one of the sharper options in the EEA and UK. Krak Card cashback can be paid in BTC instead of EUR or GBP, has no monthly subscription, and has no stated monthly cashback cap. The catch is also clear: the full 2% rate needs a GBP/EUR 50,000 balance tier, and after the welcome period that tier is based on a 30-day trailing average across Krak, Kraken, and Kraken Pro.

Disclosure: the Krak link above is a referral link. The invite page currently shows a $10 join bonus for @Tsopic, but eligibility, geography, timing, and final reward value depend on Krak's current referral terms and in-app requirements. If you sign up through it, the publisher may also receive a referral reward or commission. The link does not change the fee comparison below. Fees, rewards, eligibility, and crypto tax treatment can change. This draft was checked against public product pages on 12 May 2026 and is not financial advice.

The simple Krak cashback setup

Krak Card is a Mastercard debit card connected to the Krak Everyday balance. EU clients have EUR as the card's primary currency; UK clients have GBP. The card can spend cash and supported crypto assets according to a spend order you set in the app. If a non-primary fiat currency or crypto asset is used, Krak converts the asset into the card's primary currency when the transaction is authorized.

The reward choice matters. Krak lets cardholders receive cashback in the card's primary fiat currency or in BTC. If BTC is selected, the BTC amount is based on the BTC price when the merchant settles the transaction, not necessarily when the card was tapped. That means the BTC reward can be slightly better or worse by the time settlement happens.

The comparison: headline rate is not the answer

For European users, the main alternatives are not all solving the same job. Trading 212 is an investment-linked debit card. Revolut and Wise are strong everyday money cards, but they are not flat cashback cards. Crypto.com, Plutus, Bitpanda, Wirex, Bybit, and CEX.IO are crypto-reward cards with different token, funding, or promo mechanics. Vivid and ZEN are broader money apps with category or partner cashback. The right benchmark for Krak is therefore not "which card says the biggest number?" It is "which card gives the reward I want without adding enough friction to erase it?"

For European users, the main alternatives are not all solving the same job.

I would score each card on five things:

- Reward asset: cash, BTC, CRO, PLU, WXT, reward points, stock-linked rewards, or partner cashback.

- Real rate: the headline cashback after caps, tiers, subscriptions, and lockups.

- Fee drag: monthly fees, top-up fees, FX, ATM costs, conversion spreads, and replacement cards.

- Operational friction: balance requirements, savings-plan rules, merchant categories, or app-link tracking.

- Reward liquidity: whether the reward is usable cash/BTC or a platform token with payout rules.

Krak versus the main European reward cards

The short version: Krak is strongest for people who specifically want BTC cashback and already expect to keep meaningful assets in the Kraken/Krak ecosystem. Trading 212 is cleaner for lower-balance users who prefer invested rewards, but its cashback is capped or conditional. Revolut and Wise belong in the table because many European users already carry them, but they are mostly fee and FX tools rather than cashback tools. Crypto.com, Plutus, Wirex, and Bybit can advertise higher percentages, but the economics depend heavily on CRO, PLU, WXT, VIP tiers, caps, and conversion costs.

Use the first table for the decision. It keeps the reward, availability, headline rate, and main catch visible without forcing every fee into one row. The detailed fee notes underneath preserve the fee inventory card by card.

| Card, availability, reward | Max rate | Main catch | SkimHQ read |

|---|---|---|---|

| Krak CardEstonia in scope. | 2% | Needs a GBP/EUR 50,000 30-day average balance after the welcome period. | Best BTC-first option if you already want Kraken/Krak as a balance hub. |

| RevolutEstonia pricing is published. | 0% | Standard is a money and FX tool, not a reward card. | Strong everyday account; weak cashback benchmark. |

| WiseEstonia pricing is published. | 0% | Value comes from transparent conversion, not reward accumulation. | Best as a low-FX-cost travel and transfer card. |

| Trading 212 CardSupported European markets. | 1.5% | From 7 June 2026, the rate depends on Cashback Reinvest plus an active subscription payment. | Good if you want cashback reinvested, not BTC. |

| Crypto.com Visa CardEEA programme. | 5% | Higher tiers require subscription fees or 12-month CRO staking; lower tiers have caps. | Works best for users who already want CRO exposure. |

| PlutusSelected Europe/EEA markets. | 9% | Paid plans, rewardable-spend caps, PLU holdings, and payout fees all matter. | High headline rate, high operational friction. |

| Bitpanda CardEurozone except Cyprus and Liechtenstein. | 1% | Cashback applies only when spending eligible cryptocurrencies, not fiat or stablecoins. | Clean 1% crypto-funded cashback for Bitpanda users. |

| WirexEEA pricing exists. | 8% | Rewards are WXT and depend on Wirex plan/tier mechanics. | Crypto-app card, not a direct BTC cashback card. |

| Bybit CardEEA programme. | 10% | Points, monthly caps, VIP/spend tiers, and crypto conversion fees sit behind the headline rate. | Potentially rich, but not simple cashback. |

| CEX.IO CardEstonia in scope. | Variable | Rewards are promotional/random rather than a stable fixed cashback rate. | Occasional crypto rewards, not a predictable daily-driver card. |

| VividSelected European markets. | 4% | Requires account balance/assets, selected categories, country availability, and plan terms. | Useful for category optimizers, not BTC stackers. |

| ZEN.COMSupported EEA markets. | Offer-based | Purchase must start from the ZEN app cashback link; Free plan may halve values. | Partner-shopping cashback, not all-spend rewards. |

Fee detail by card

This is the fee audit behind the scan table. Krak remains the cleanest BTC comparison, but each alternative has a different fee pattern: monthly plan costs, ATM limits, FX, token conversion, or in-app funding charges.

Krak CardBTC or EUR cashback, EEA + UK

- Monthly and card fees

- No monthly fee. Virtual and plastic cards are free. Plastic replacement is GBP/EUR 4.99; metal replacement is GBP/EUR 60.

- ATM and FX

- No Krak ATM fee, but third-party ATM fees may apply. No Krak FX markup on card spend; Mastercard rate applies.

- Crypto and funding

- Crypto spending includes conversion spread. Near-instant Apple Pay, Google Pay, and debit/credit card deposits cost USD 0.25 plus 3.75%. Instant buy/sell/conversion is 1%; small balance conversion is 3%; crypto withdrawals vary by asset.

- Reward caveat

- 2% requires a GBP/EUR 50,000 30-day average balance after the welcome period. Rewards appear after merchant settlement.

RevolutEveryday EUR and FX card, Estonia pricing published

- Monthly and card fees

- Standard subscription is free. First Standard card is free but delivery applies; replacement card is EUR 6 plus delivery. Virtual cards are free.

- ATM

- ATM withdrawals are free up to 5 withdrawals or EUR 200 per rolling month, then 2% with a EUR 1 minimum.

- FX and funding

- Standard has a EUR 1,000 monthly exchange limit before fair-use fees. Weekend exchange has a 1% fee; after the Standard exchange limit, a 1% fair-use fee applies. Adding money with non-EEA or commercial cards may carry an in-app fee.

- Reward caveat

- No flat personal-card cashback on Standard. Revolut Pro cashback is separate from everyday consumer debit-card cashback.

WiseLow-FX-cost debit card, Estonia pricing published

- Monthly and card fees

- No subscription. For Estonia residents, physical card is EUR 7; digital card is free; replacement card is EUR 4; express delivery starts from EUR 10.40.

- ATM

- Wise Estonia pricing lists free ATM withdrawals up to EUR 250 per month, then 2.69% of the amount over EUR 250.

- FX and wallet funding

- Spending same-currency balances is free. If Wise converts, conversion fees apply and start from 0.47% on the Estonia pricing page checked. Topping up external e-wallets can cost 2%.

- Reward caveat

- No cashback; Wise competes on conversion transparency.

Trading 212 CardInvested cashback in supported European markets

- Monthly and card fees

- No monthly subscription for the card itself. A one-time physical card issue charge applies.

- ATM and FX

- ATM withdrawals are free up to EUR 400 per month outside the UK, then 1%. Card transactions have 0% FX fee; converting funds in the app has a 0.15% FX fee.

- Reward caveat

- From 7 June 2026, the 1.5% rate requires Cashback Reinvest plus an active monthly, bi-weekly, or weekly subscription payment detected on the card.

Crypto.com Visa CardCRO rewards in supported European/EEA markets

- Monthly, staking, and caps

- Free Midnight Blue tier has 0% everyday CRO rewards. Higher tiers require monthly/yearly subscription fees or 12-month CRO staking. Published caps include USD 25 per month for Ruby and USD 75 for Jade/Indigo; higher tiers can have no everyday rewards cap.

- ATM and limits

- Free monthly ATM allowance ranges from EUR 200 to EUR 1,000 depending on tier. Monthly ATM withdrawal cap is EUR 10,000. Aggregated top-up limit is EUR 25,000 per day/month and EUR 250,000 per year in the Europe fee table checked.

- Other fees

- The official fee article points users to the applicable cardholder agreement for jurisdiction and tier-specific charges, so replacement, inactivity, and exchange details should be checked inside the app.

PlutusPLU rewards in selected Europe/EEA markets

- Monthly and reward caps

- Starter is GBP/EUR 6.99 per month, Everyday is GBP/EUR 9.99, and Premium is GBP/EUR 19.99, subject to current promotions. Rewardable card spend is GBP/EUR 250 per month on Starter, 500 on Everyday, and 1,000 on Premium before reward-level boosts.

- Card, trading, and payout

- Virtual card order is free; physical card order is GBP/EUR 9.99. Starter has a 1% trading fee; Everyday and Premium show 0%. PLU reward payout has dynamic gas and service fees.

- POS and ATM

- Domestic POS transactions are free; non-domestic POS transactions are 2.5%; ATM withdrawals are 2.5%.

Bitpanda Card1% crypto-funded cashback, Estonia in scope

- Reward and conversion

- Each Bitpanda Card payment triggers an asset-to-fiat trade and incurs the usual Bitpanda trading fee. Cashback does not apply when spending fiat balances, stablecoins, precious metals, or Bitpanda Stocks.

- ATM and FX

- ATM withdrawals cost 2% of the withdrawal or at least EUR 2. Payments and withdrawals in non-EUR currencies no longer incur Bitpanda fees, though local ATM fees can still apply.

- Crypto fee reference

- Bitcoin buy/sell premiums on Bitpanda are listed at 0.99% on the fee page checked.

WirexWXT rewards, EEA pricing published

- Monthly and reward mechanics

- Standard plan is listed at EUR 0/month. Standard pricing shows up to 1% Cryptoback on card purchases, while higher advertised levels depend on plan and WXT-related mechanics.

- Exchange and top-up

- Wirex says exchange fees vary by currency pair and can be viewed in-app. Local-card funding can cost 0% or more depending on top-up currency and country/region.

- ATM and limits

- The card page advertises fee-free ATM allowance, while Wirex fee and limit pages tell users to check region-specific limits and in-app details.

Bybit CardPoints and Auto Cashback in the EEA programme

- Card fees

- No annual, inactivity, or cancellation fee is listed in the card fee table. Virtual card issuance and replacement are free; physical card is EUR/USD 5 in the EEA table checked.

- FX and crypto conversion

- EEA foreign exchange fee is 0.5% on top of Mastercard's rate. Crypto conversion fee is 0.9% on top of Bybit's One-Click Sell exchange rate, with a minimum conversion amount.

- Reward caveat

- Auto Cashback must be enabled. Points/cashback are capped by tier, processed daily, and converted at redemption rates.

CEX.IO CardEEA card with promotional crypto rewards

- Availability and promo rules

- CEX.IO says the card is available for EEA residents. The cashback promo requires qualifying online or in-store purchases of at least EUR 1.

- Fees to verify

- The support articles checked focus on card availability and the cashback promo, not a full stable public card-fee schedule. Verify card, conversion, and withdrawal costs inside CEX.IO before relying on it as a daily cashback card.

- Reward caveat

- Rewards are determined by CEX.IO's randomization/program rules and promotions can change.

VividCategory cashback in selected European markets

- Monthly and plan fees

- Standard is EUR 0 per month for active customers, otherwise EUR 3.90 account management fee. Plus is EUR 6.90 per month; Prime was listed from EUR 7.90 per month after a one-month trial.

- Card fees

- Physical card issue is listed at EUR 19.90. Virtual card issue is EUR 1 on Standard and Plus; Prime includes one free virtual card and charges EUR 1 for each additional card. Standard charges EUR 0.99 monthly for each additional physical or virtual card.

- Investing, FX, and crypto

- Money market fund service fee is 1% on Standard, 0.70% on Plus, and 0.30% on Prime. Card/invest FX markup is shown at 0.25%. Crypto trading starts at 2% on Standard, 1% on Plus, and 0.75% on Prime. Stock and ETF trading is EUR 1 per trade.

- Reward caveat

- Cashback for the next month requires at least EUR 1,000 account balance or EUR 100 in assets on the last day of the current month.

ZEN.COMPartner cashback in supported EEA markets

- Monthly and card fees

- Pricing checked showed Free at EUR 0, Gold at EUR 0.90 per month, Platinum at EUR 6.90 per month, and Pro at EUR 6.90 per month under a limited promo. Physical card ordering can be EUR 10 on Free, while paid plans include at least one or more physical cards depending on plan.

- ATM

- ATM withdrawals: Free 1.5%; Gold free up to EUR 200 per month then 1.5%; Platinum and Pro free up to EUR 800 per month then 1.5%.

- Top-up and FX

- EEA individual card top-ups are 0.5% on Free and 0% on Gold/Platinum/Pro. Non-EEA individual and business card top-ups run 3% on Free, 2.75% on Gold, and 2.5% on Platinum/Pro. Currency exchange minimum margins start from 0.60% on Free, 0.30% on Gold, and 0.10% on Platinum/Pro.

- Reward caveat

- Free plan users can see cashback values reduced by 50%. Purchase must usually start from the ZEN app cashback link and be paid with a ZEN Card.

The practical winner depends on what you want to earn

If the goal is BTC cashback, Krak is the cleanest pick in this comparison because BTC is a native payout option and the top rate is 2%. Bitpanda can pay crypto cashback when purchases are funded with eligible cryptocurrencies, but the rate is 1% and card spending triggers an asset-to-fiat trade. Crypto.com, Plutus, and Wirex can look larger on paper, but the reward asset is CRO, PLU, or WXT, not BTC. Bybit can show higher percentage cashback tiers, but the reward system uses points, tier caps, and redemption mechanics.

If the goal is BTC cashback , Krak is the cleanest pick in this comparison because BTC is a native payout option and the top rate is 2%.

If the goal is fiat-style simplicity, Trading 212 is easier to reason about for users who want invested rewards instead of crypto rewards. Trading 212's 1.5% rate is becoming conditional on Cashback Reinvest and an active subscription payment. Revolut and Wise are even simpler for travel and currency conversion, but they should be treated as low-friction payment cards rather than cashback cards.

If the goal is maximum advertised percentage, the answer shifts toward Crypto.com, Plutus, Wirex, Bybit, Vivid, or ZEN, but only after reading the mechanics. The extra percentage often comes from token exposure, subscription tiers, partner stores, categories, or plan-specific limits. That can still be valuable, but it is a different product than "tap card, receive BTC."

LIKE WHAT YOU'RE READING?

The digest delivers 3–5 scored business ideas every morning — graded, sourced, and ready to act on.

How to use Krak without letting fees eat the reward

The best way to preserve cashback value is to avoid unnecessary conversion and funding costs. For a European user choosing BTC cashback, that means funding in EUR when possible, keeping the spend order deliberate, and understanding when crypto will be sold to settle a card transaction. If you want to stack BTC, block BTC from the spend order and spend EUR instead; otherwise you may be selling the same asset you are trying to accumulate.

- Use bank/wire funding where available instead of near-instant card or wallet deposits that carry the USD 0.25 plus 3.75% fee.

- Keep the card's primary EUR balance funded for daily purchases to avoid unnecessary crypto conversion spreads.

- Select BTC as the cashback payout asset only if you accept BTC price movement between purchase and merchant settlement.

- Do not chase the 2% tier unless the GBP/EUR 50,000 average balance already fits your broader portfolio plan.

- Review excluded transactions: ATM withdrawals, refunds, chargebacks, very small transactions, and non-purchase transactions do not qualify for Krak cashback.

FAQ: Krak cashback balance and timing

Do I need to keep a balance to receive any cashback?

No. Krak's cashback overview says all Krak Cardholders automatically earn cashback, with no subscription, opt-in, or minimum balance required. The balance requirement is about moving into higher cashback tiers, not about qualifying for cashback at all.

Why might I not get 2% immediately after depositing EUR 50,000?

During the first 30 days as a new customer, Kraken says users receive Max tier benefits as a welcome gift. After that period, the tier is based on a 30-day trailing average, not just the live balance. If you go from EUR 0 to EUR 50,000, your average needs time to catch up before the account naturally qualifies for the 2% tier again.

Does the balance have to sit only in Krak?

No. Krak says the total balance is calculated across Krak, Kraken, and Kraken Pro combined. The practical question is whether those assets are part of your broader plan anyway, because chasing a cashback tier by holding too much idle balance can be a poor trade.

Are the funds locked?

Krak's reward-balance page describes tier calculation, not a lockup. You can move funds, but after the first 30 days your tier follows the rolling average. That means spending or withdrawing can lower a future tier, while a new deposit may need time before it fully affects the average.

When does the BTC cashback appear?

Cashback appears after the merchant settles the transaction. Until settlement, the reward can show as pending. If BTC is selected as the payout asset, Krak converts the cashback at the BTC price when the merchant settles, so the exact BTC amount can move with the market between purchase and settlement.

What does the @Tsopic referral link give?

The Krak invite page for @Tsopic currently displays a $10 join bonus and says to use @Tsopic as the invite code when signing up. The important caveat is that the bonus is available only in eligible geographies and under Krak's active referral terms. Kraken's referral terms also say rewards are subject to eligibility checks, promotional limits, and timing after verification, so treat the displayed amount as a current offer rather than a permanent guarantee.

Founder signal: cashback is retention infrastructure

For SkimHQ, the interesting part is not only which card pays the most. Cashback cards show how fintechs turn occasional app usage into daily behavior. Krak's design connects custody, spend, and rewards. Trading 212 connects spend to investing. Crypto.com, Plutus, Wirex, Bybit, Bitpanda, and CEX.IO connect spend to crypto ecosystems. ZEN and Vivid connect spend to partner marketplaces and plan upgrades.

That creates a clean startup wedge: consumers need a fee-aware reward optimizer that explains the real reward after caps, FX, subscriptions, balance requirements, and token liquidity. The buyer pain is obvious because the pages are not directly comparable. The first wedge could be a Europe-only card rewards monitor, a browser/app companion for partner cashback, or a compliance-friendly affiliate layer that ranks cards by effective reward instead of advertised rate.

The lesson is durable: when the reward is financial, clarity is the product. Users do not need another percentage. They need to know which habit actually compounds after fees.

Sources checked

- Krak Card product page, Krak Card cashback overview, and Krak reward balances guide.

- Krak pricing page and Krak Card FAQs.

- Krak @Tsopic invite page and Krak Referral Program terms.

- Revolut Estonia Standard fees and Revolut Estonia plan comparison.

- Wise Estonia card fees and Wise Estonia pricing page.

- Trading 212 Card page, 212 Card fee article, and cashback programme update.

- Crypto.com EEA card tiers and Crypto.com Europe fees and limits.

- Plutus plans and Plutus fees and limits.

- Bitpanda Card guide, Bitpanda Card cashback applicability, and Bitpanda fee guide.

- Wirex EEA pricing, Wirex Cryptoback explanation, and Wirex fees page.

- Bybit Card rewards guide, Bybit Card fees and limits, and Bybit Card rewards FAQ.

- CEX.IO Crypto Card guide and CEX.IO Card cashback promo guide.

- Vivid cashback page and Vivid personal plans page.

- ZEN pricing plans, ZEN card fee article, and ZEN Instant Cashback guide.

SkimHQ tracks source-backed income plays and fintech wedges where the real opportunity is clearer than the headline. Subscribe for more practical comparisons with buyer logic attached.

Subscribe now ->SkimHQ tracks source-backed income plays and fintech wedges where the real opportunity is clearer than the headline.